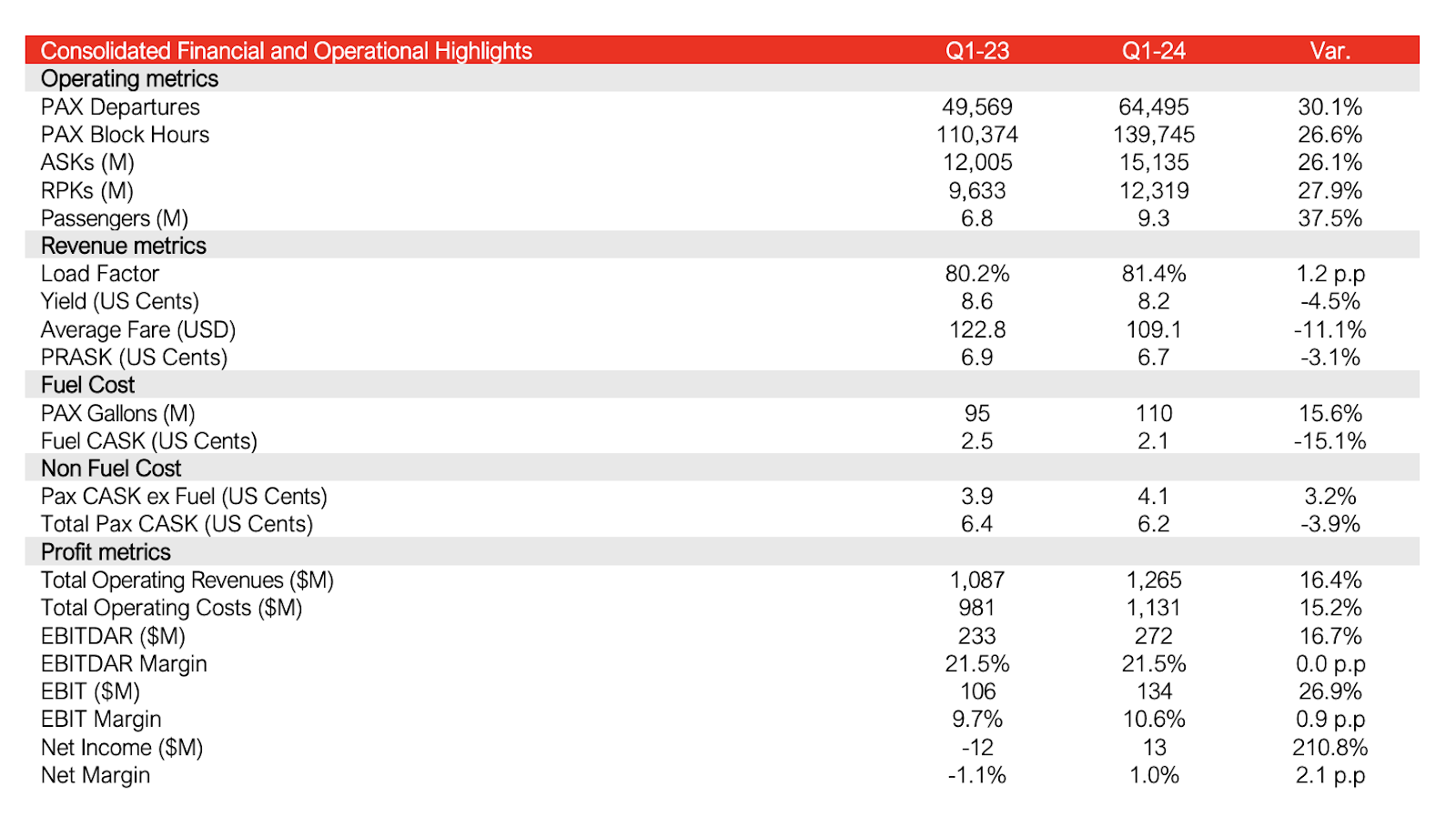

Avianca Group International Limited affiliated passenger airlines (“AGIL”, “the Group” or “the Company”) reported its first quarter 2024 results. Avianca’s capacity increased by 26.1% year-over-year, with a robust load factor of 81.4%, 1.2 percentage points higher than first quarter 2023, and a 37.5% increase in transported passengers, reaching 9.3 million.

The Company posted $272 million in EBITDAR at a 21.5% margin during first quarter 2024, 16.3% ahead of the same period in 2023. For the period, Net Income was $13 million.

“We remain committed to transporting our customers to more destinations in an affordable way,” said Frederico Pedreira, Avianca’s Chief Executive Officer. “In the first quarter, we introduced a new, more simplified and flexible fare scheme that allows our customers to fly according to their needs, and we continued to expand our network and improve our connectivity with the launch of new routes, including the reopening of Bogota-Paris, after 20 years, as well as Bogota-Montreal. We achieved this while delivering solid operating results, demonstrating our commitment to transporting our clients safely, on time and with their baggage. For all the achievements, I would like to thank our team for their commitment and the outstanding work they continue to do”.

Photo: Avianca – EmiroMejia@2009

First Quarter 2024 Highlights

Consolidated capacity, measured in Available Seat Kilometers (ASK), reached 15,135 million in the first quarter of 2024; a 26.1% increase relative to first quarter 2023. The Group transported 9.3 million passengers during the period, representing a 37.5% increase over the same period in 2023.

Total operating revenues in the first quarter of 2024 reached $1,265 million; a 16.4% increase over the same period in 2023, while total operating expenses were $1,131 million, a 15.2% increase over the same period in 2023, in spite of a 26.1% capacity increase.

EBITDAR was $272 million in the first quarter of 2024, at a 21.5% margin, while Net Income for the period was $13 million.

Our cash balance was $971 million at March 31, 2024.

Passenger revenues were $1,013 million for the first quarter of 2024, reflecting a 22.2% increase relative to first quarter 2023. This increase is a result of the Company’s continued efforts to make flying more accessible to a broader range of passengers.

Cargo, Loyalty and other revenues for the first quarter of 2024 were $252 million. Quarterly LifeMiles Cash EBITDA increased 15.3% relative to first quarter 2023, reaching $36 million. Cargo revenues during the period were $152 million, an 8.3% decrease relative to first quarter 2023 due to continued market softening and industry freighter capacity remaining above prepandemic levels. However, Cargo revenues were ahead of Business Plan.

Net Debt to last-twelve-month EBITDAR was 3.2x.

Passenger Costs per Available Seat Kilometer excluding fuel (PAX CASK ex-fuel) in the first quarter of 2024 was $4.1 cents.

We ended the first quarter of 2024 with an operating passenger fleet comprised of 141 aircraft: 128 Airbus 320 family aircraft, and 13 Boeing 787s.

Avianca reintroduced Business Class service on the Narrowbody operation from Bogota to 11 destinations in the Americas: Chile, São Paulo, Buenos Aires, Montevideo, Río de Janeiro, Miami, Washington, New York, Boston, Toronto, and Mexico City. The service will be available starting July 1st.

Avianca resumed the Bogota-Caracas route, and announced 5 new routes from Medellin to Buenos Aires, Santiago, and Lima; and from Bogota to Montreal, and Paris. In the first quarter of 2024, our network consisted of 150 routes connecting 76 destinations.

Avianca’s first reconfigured B787 started operations the third week of April, with number of seats increased from 250 to 291. offering 16.4% additional cabin capacity. We are on track to complete the reconfiguration of our remaining 12 widebody aircraft this year.

Avianca Cargo continued to lead the flower market from Colombia to the US during Valentine’s season, transporting ∼18,000 tons of flowers in over 300 cargo flights from Colombia and Ecuador, while further strengthening its competitive position within the region.

Also, Avianca Cargo won the ESG Award during the Aviation Achievement Awards 2024, reflecting its commitment to sustainability.

LifeMiles announced new policies that make it easier for customers to qualify for Elite status.

Swiss International Air Lines (SWISS) has reported an operating result (Adjusted EBIT) of CHF 30.7 million for the seasonally weak first quarter of 2024. The result is some CHF 48 million below the prior-year period (Q1 2023: CHF 78.4 million). Total first-quarter revenues for 2024 amounted to CHF 1.2 billion, up 8.1 per cent on their prior-year level.

“As anticipated, the exceptional market conditions that our industry experienced immediately after the pandemic have continued to fade,” explains SWISS Chief Financial Officer Markus Binkert. “Demand for travel remains high. But many airlines have further increased their capacities. This is tending to bring yields down from their prior-year levels – at our company, too. We have also seen a sizeable weakening in our air cargo business, which benefited from particularly strong tailwinds during COVID times.”

SWISS’s first-quarter earnings were also reduced by rising costs. In addition to the adverse effects of inflation and higher fuel prices, a rise in personnel costs was particularly felt as the terms of the new collective labour agreements for cockpit and cabin personnel were reflected in staff expense.

“Given that the first quarter of the year tends to be one of the weaker ones for seasonal reasons, we are satisfied with this earnings result,” CFO Binkert continues. “Our business has returned to normality at a high level. For our full-year results, though, the next two seasonally strong quarters will be key.”

Focus on stability and punctuality in the peak travel season

Having delivered a solid business and operating performance over the Easter period, SWISS is now preparing for the busy summer travel months. In doing so, the company is putting customer satisfaction firmly centrestage.

“Last year we were Europe’s stablest airline,” CEO Dieter Vranckx explains. “We want to be so this summer, too, and offer our customers the kind of reliability that they should be able to expect from us. For a premium airline like ours, though, stability alone is not enough. So this year we aim to substantially improve our flights’ punctuality as well, in collaboration with our partners. To this end we have launched a companywide programme that is firmly focused on the satisfaction of our customers. We’re already working intensively on this, and are developing a wide range of actions to help us achieve these objectives.”

Passenger volume growth

SWISS transported some 3.7 million passengers in the first three months of 2024 – just under 17 per cent more than in the same period last year. Almost 31,000 flights were operated in the period, a 14.5-per-cent increase on the first quarter of 2023. Systemwide, first-quarter production was raised 11.6 per cent in available-seat-kilometre terms. Total first-quarter traffic volume, measured in revenue passenger-kilometres, was up 11.3 per cent. Systemwide seat load factor for the first-quarter period stood at 80.7 per cent, down 0.2 percentage points from its prior-year level.

Group revenue increases by 5 percent to 7.4 billion euros in the first quarter

Number of passengers rises to 24 million in the first quarter

Adjusted EBIT in the first quarter at -849 million euros

Strikes impact earnings by around 350 million euros in the first quarter

Unit costs excluding strike impact below previous year

Summer with record number of holiday destinations and 16 percent more bookings than last year

Adjusted EBIT of around 2.2 billion euros expected for the full year of 2024

Carsten Spohr, Chairman of the Executive Board and CEO of Deutsche Lufthansa AG:

“We are now leaving the first quarter behind us, which was mainly impacted by strikes, and are at a turning point. We have reached long-term wage agreements for the majority of our employees. This means planning certainty and clarity for the coming years. We are still seeing strong demand, which is even significantly higher than last year for the summer. We are therefore continuing to expand our offering and are growing on long-haul routes in particular. Our planes remain well filled throughout. One thing is already clear: it will be another very strong summer. I am particularly pleased that we are continuing to see a positive trend not only among leisure but also business travelers. We are now devoting all our energy to further expanding our premium customer offers and ensuring punctual and reliable flight operations.”

Results for the first quarter of 2024

The Group increased its revenue by five percent year-on-year to 7.4 billion euros in the first quarter of 2024 (previous year: 7.0 billion euros). The Lufthansa Group recorded an operating loss (Adjusted EBIT) of 849 million euros (previous year: -273 million euros). Strikes, both by various employee groups within the Group and by employees of our system partners, had a negative impact of around 350 million euros on earnings. In addition, Lufthansa Cargo’s result declined now that the logistics industry has returned to normal after the pandemic-related exceptional economic situation. The Adjusted EBIT margin fell to -11.5 percent (previous year: -3.9 percent). The Group result fell to -734 million euros (previous year: -467 million euros).

Passenger numbers and traffic development

Demand for air travel continued to rise in the first quarter of the current year. A total of 24 million passengers flew with the airlines of the Lufthansa Group, an increase of 12 percent compared to the previous year (Q1 2023: 22 million). The Group airlines expanded their seat capacity by 12 percent year-on-year despite the strike-related flight cancellations. Compared to the pre-Crisis year 2019, this was 84 percent, around 5 percentage points lower than originally planned. Despite the significant increase in capacity, the load factor remained consistently high due to high demand. The passenger load factor amounted to 79.7 percent and was thus at the previous year’s level.

Strikes have a significant negative impact on Passenger Airlines’ earnings

The Lufthansa Group Passenger Airlines’ revenue rose by seven percent to 5.6 billion euros in the first quarter (previous year: 5.2 billion euros). They recorded an Adjusted EBIT of -918 million euros (previous year: -512 million euros). Strikes had an impact of around 300 million euros on earnings in this segment.

Yields fell by 2.5 percent compared to the previous year, partly due to the strike-related uncertainty on the customer side and the corresponding lack of high-priced last-minute bookings. Unit revenues (RASK) were 6.3 percent down on the previous year, also influenced by lower cargo revenues and significantly higher compensation payments to passengers due to the strike.

Unit costs (CASK) rose by 2.9 percent compared to the same quarter of the previous year due to the strike. Adjusted for the strike effects, however, they were 1.8 percent below the previous year despite higher expenses for fees, MRO and personnel.

Due to the high losses in the core brand Lufthansa in the first quarter (Adjusted EBIT -640 million euros), Lufthansa Airlines has initiated measures to strengthen the result this year in the short term. Among other steps, it is planned to reduce operating costs, stop new projects and assess the need for additional staff in administrative areas.

Lufthansa Technik benefits from more air traffic

Demand for maintenance, repair and overhaul services as well as other Lufthansa Technik products increased in the first quarter of 2024 due to the positive trend in air travel. Revenue increased accordingly by 15 percent year-on-year to 1.8 billion euros (previous year: 1.5 billion euros). Adjusted EBIT fell by 14 percent to 116 million euros (previous year: 135 million euros), impacted by strike-related work stoppages. Excluding this effect, which had a negative impact on earnings of around 25 million euros, earnings were up on the previous year.

In the logistics business, capacity rose by seven percent due to the expansion of air traffic and revenue tonne-kilometres also increased by ten percent. Yields were around 25 percent lower than in the same quarter of the previous year, in which the result was significantly boosted by high demand due to supply chain disruptions and the shortage of capacity as a result of the pandemic. Lufthansa Cargo thus achieved an Adjusted EBIT of -22 million euros (previous year: 151 million euros). Excluding the strike effects of 25 million euros, the quarterly result was slightly positive.

Positive Adjusted free cash flow further reduces net debt

Due to the continued high level of incoming bookings, operating cash flow amounted to around 1.3 billion euros despite the negative operating result. At 940 million euros, net investments were around ten percent below the previous year, meaning that Adjusted free cash flow amounted to 305 million euros (previous year: 482 million euros).

The Group further strengthened its balance sheet in the first quarter of 2024. Net debt decreased to 5.5 billion euros compared to the end of 2023 (December 31, 2023: 5.7 billion euros) due to the positive free cash flow. Net pension obligations fell to 2.4 billion euros due to a higher discount rate (December 31, 2023: 2.7 billion euros). At the end of March 2023, the company had liquidity totaling 10.8 billion euros (December 31, 2023: 10.5 billion euros) at its disposal. Following an upgrade by Moody’s in the first quarter, the Lufthansa Group is now the only European network airline to be consistently rated investment grade again by all four agencies in the market.

Remco Steenbergen, Chief Financial Officer of Deutsche Lufthansa AG:

“We cannot be satisfied with the operating result for the first quarter; at more than 350 million euros, the various strikes had a significant impact on our result. Nevertheless, cash flow was positive due to the continuing high demand for air travel. We were also able to further strengthen our balance sheet. In the coming months, we will work intensively to compensate for the effects of rising costs. We have taken additional measures to this end, particularly at Lufthansa Airlines, which is significantly affected by rising personnel expenses and fees. I therefore remain convinced that we will be able to achieve stable unit cost development for the year as a whole without taking the strikes in the first quarter into account.”

Bookings for summer 16 percent up on previous year

Global demand for air travel remains strong, particularly from private travelers. The company expects another very good summer of travel. Never before have so many holiday destinations been served by Lufthansa Group airlines as this year. The most popular summer destinations in 2024 are once again Spain, Portugal, Italy and Greece and, for long-haul travel, the USA, Japan and Southern Africa. This year, many holidaymakers will once again be able to afford a ticket in one of the premium classes. In addition to the very good demand in the private travel segment, the trend in the business travel segment is also positive. This applies in particular to long-haul flights. The Lufthansa Group is continuously expanding its offering here. In addition to the traditionally strong North American routes, demand from business travelers on the India and Japan routes in particular is growing this year.

Overall, bookings for the summer timetable (April to October) are 16 percent up on the previous year.

Guests can now also enjoy Lufthansa Allegris, the new travel experience on long-haul routes. Allegris will start regular scheduled service on May 1. The first Airbus A350-900 equipped with Allegris will fly from Munich to Vancouver on the Canadian West Coast. The second destination is Toronto, which will be served alternately with Vancouver on selected flights in the first few months. With further A350s delivered, the Allegris cabin will also be used on flights to Chicago and Montreal in the summer.

Financial outlook

The Lufthansa Group plans to increase available capacity in the second quarter to around 92 percent of the pre-crisis level. The increase will therefore be lower than originally planned due to further investments in operational stability and delayed aircraft deliveries. The company expects a year-on-year decline in unit revenues (RASK) in the low single-digit percentage range, partly because customers were reluctant to make short-term bookings for April and, to a lesser extent, May during the wage disputes that have now been resolved. Unit costs (CASK) are expected to increase in the low single-digit percentage range in the second quarter. Adjusted EBIT in the second quarter will therefore still be below that of the previous year. In line with the lower capacity in the first two quarters, the Lufthansa Group now expects to achieve a capacity level of around 92 percent of the pre-crisis figure for 2019 (previously: 94 percent) for the full year 2024.

In the third quarter, capacity is to be increased further to over 95 percent of the pre-crisis level. Based on incoming bookings, the Group airlines expect unit revenues (RASK) in the third quarter to be higher than in the previous year.

In the second half of the year, the Group’s operating result is expected to be higher than in the previous year. As already communicated on April 15, Adjusted EBIT for the full year is now expected to be around 2.2 billion euros (previously: stable earnings development compared to 2.7 billion euros in the previous year). For the Passenger Airlines, a decline in unit revenues (RASK) in the low single-digit percentage range and an increase in unit costs (CASK), also in the low single-digit percentage range, are expected for the full year. Excluding the effects of the strikes in the first quarter, unit costs (CASK) are expected to remain stable. Adjusted free cash flow is expected to be at least 1 billion euros (previously: at least 1.5 billion euros).

Further information

Further information on the results of individual business units will be published in the report on the first quarter of 2024. This will be published at the same time as this press release on April 30, 2024 at 07:00 CEST at www.lufthansagroup.com/investor-relations.

Condor has taken delivery of its first Airbus A320neo (D-ANCZ) on lease from Avolon following an event in Toulouse.

The new aircraft is part of the airline’s ongoing fleet modernization which already includes the A330neo for long-haul routes. By operating aircraft from the A320 and the A330neo families, Condor will fully benefit from the advantages of commonality between these two aircraft family types.

Condor has operated the A320 family on its European route network for more than 20 years. With the introduction of the A320neo, Condor is building on this wealth of experience and benefiting from additional efficiency and comfort advantages the A320neo offers.

The new A320neo fleet will be powered by Pratt & Whitney engines and offer passengers maximum comfort with Airbus’ unique Airspace cabin. At the end of March 2024, the A320neo family had won more than 10000 orders from over 130 customers.

American Airlines Group Inc. (NASDAQ: AAL) today reported its first-quarter 2024 financial results, including:

Record first-quarter revenue of approximately $12.6 billion.

First-quarter net loss of $312 million, or ($0.48) per diluted share. Excluding net special items1, first-quarter net loss of $226 million, or ($0.34) per diluted share.

Generated operating cash flow of $2.2 billion and free cash flow2 of $1.4 billion in the first quarter.

Reduced total debt3 by nearly $950 million in the first quarter. The company is now more than 80% of the way to its 2025 total debt reduction goal.

“The American Airlines team continues to build a reliable, efficient and resilient airline,” said American’s CEO Robert Isom. “While we aren’t satisfied with our first-quarter financial results, we have a strong foundation in place, and we remain on track to deliver on our full-year financial targets. Our team is running a fantastic operation, driving revenue through our commercial initiatives, efficiently managing costs, and producing free cash flow to further strengthen our balance sheet.”

Resources

Operational performance

American is running the best operation in its history because of a steadfast commitment to operational excellence and strong collaboration across the entire airline. The company produced its best-ever first-quarter completion factor and improved its mishandled baggage rate year over year. American achieved these results despite air traffic control challenges and significant weather events across its network during the quarter.

Financial performance

American produced results within previously guided ranges for each of its operating metrics despite a significant increase in the cost of fuel in the quarter. The company generated record first-quarter revenue of approximately $12.6 billion and a GAAP operating margin of 0.1%. Excluding the impact of net special items1, American produced an operating margin of 0.6% in the first quarter.

Balance sheet

Strengthening the balance sheet remains a top priority for American. In the first quarter, the company reduced total debt3 by nearly $950 million and has now achieved more than $12 billion, or over 80%, of its goal of reducing total debt3 by $15 billion by the end of 2025.

Guidance and investor update

Based on present demand trends and the current fuel price forecast and excluding the impact of special items, the company expects its second-quarter 2024 adjusted earnings per diluted share4 to be between $1.15 and $1.45. The company continues to expect its full-year adjusted earnings per diluted share4 to be between $2.25 and $3.25.

Notes

See the accompanying notes in the financial tables section of this press release for further explanation, including a reconciliation of all GAAP to non-GAAP financial information and the calculation of free cash flow.

The company recognized $86 million of net special items in the first quarter after the effect of taxes, which included operating net special items of $70 million, principally related to one-time charges resulting from the ratification of a new collective bargaining agreement for its passenger service team members represented by the CWA-IBT, as well as nonoperating net special items of $46 million for charges associated with mark-to-market net unrealized losses on certain equity investments.

Please see the accompanying notes for the company’s definition of free cash flow, which is a non-GAAP measure.

All references to total debt include debt, finance and operating lease liabilities and pension obligations.

Adjusted earnings per diluted share guidance excludes the impact of net special items. The company is unable to reconcile certain forward-looking information to GAAP as the nature or amount of net special items cannot be determined at this time.

American AIrlines aircraft photo gallery (Boeing):

Southwest Airlines Company today reported its first quarter 2024 financial results:

Net loss of $231 million, or $0.39 loss per diluted share

Net loss, excluding special items1, of $218 million, or $0.36 loss per diluted share

Record first quarter operating revenues of $6.3 billion

Liquidity2 of $11.5 billion, well in excess of debt outstanding of $8.0 billion

Bob Jordan, President and Chief Executive Officer, stated, “While it is disappointing to incur a first quarter loss, we exited the quarter with healthy profits and margins in the month of March. We are focused on controlling what we can control and have already taken swift action to address our financial underperformance and adjust for revised aircraft delivery expectations. I want to thank our more than 74,000 Employees for their continued Warrior Spirit to maintain a reliable and resilient operation as we adapt to aircraft delivery constraints and adjust to slower than planned growth for this year and next.

“Our first quarter 2024 revenue performance, while shy of our prior aspirations, resulted in record first quarter operating revenues, record first quarter passengers carried, and a solid sequential improvement in nominal unit revenue when compared with seasonal norms. The sequential improvement was driven by an acceleration in managed business revenues as well as benefits from network adjustments, which started in earnest with the March schedule. While costs remain a headwind, we are realizing benefits from our ongoing cost reduction actions and remain focused on enhancing productivity and controlling discretionary spending. We also have certainty with labor rates, having ratified agreements with 11 of our labor groups in the past 18 months, including the agreement ratified yesterday for our Flight Attendants.

“Achieving our financial goals is an immediate imperative. The recent news from Boeing regarding further aircraft delivery delays presents significant challenges for both 2024 and 2025. We are reacting and replanning quickly to mitigate the operational and financial impacts while maintaining dependable and reliable flight schedules for our Customers.

“To improve our financial performance, we have intensified our network optimization efforts to address underperforming markets. Consequently, we have made the difficult decision to close our operations at Bellingham International Airport, Cozumel International Airport, Houston’s George Bush Intercontinental Airport, and Syracuse Hancock International Airport. I want to sincerely thank our Employees, the airports, and the communities for all their incredible support over the years.

“Additionally, we are evaluating options to enhance our Customer Experience as we study product preferences and expectations, including onboard seating and our cabin. And, we are implementing cost control initiatives, including limiting hiring and offering voluntary time off programs. We now expect to end 2024 with approximately 2,000 fewer Employees as compared with the end of 2023.

“We are focused on achieving our financial prosperity goals and creating value for our Shareholders, while we adjust to changes in our aircraft delivery plans, Customer travel patterns and preferences, higher fuel prices, and other cost pressures. We are excited and optimistic with a robust set of strategic initiatives that are well underway. They are comprehensive and aimed at enhancing the Customer Experience; delivering operational excellence; creating new and meaningful revenue opportunities; expanding margins; and achieving return on invested capital well above of our weighted average cost of capital. We look forward to sharing these plans at our Investor Day in September.”

(a) Operating revenue per available seat mile (“RASM” or “unit revenues”).

(b) Available seat miles (“ASMs” or “capacity”). The Company’s flight schedule is published for sale through March 5, 2025. The Company expects third quarter 2024 capacity to increase in the low-single digits and fourth quarter 2024 capacity to decrease in the low- to mid-single digits, resulting in capacity growth in the range of flat to down low-single digits in second half 2024, all on a year-over-year percentage basis.

(c) Operating expenses per available seat mile, excluding fuel and oil expense, special items, and profitsharing (“CASM-X”).

(d) Aircraft on property, end of period. The Company now plans for approximately 20 Boeing 737-8 (“-8”) aircraft deliveries and 35 aircraft retirements in 2024, comprised of 31 Boeing 737-700s (“-700”) and four Boeing 737-800s (“-800”). This is compared with its previous plan for approximately 46 -8 deliveries and 49 aircraft retirements. The delivery schedule for the Boeing 737-7 (“-7”) is dependent on the Federal Aviation Administration (“FAA”) issuing required certifications and approvals to The Boeing Company (“Boeing”) and the Company. The FAA will ultimately determine the timing of the -7 certification and entry into service, and Boeing may continue to experience manufacturing challenges, so the Company offers no assurances that current estimations and timelines will be met.

Revenue Results and Outlook:

First quarter 2024 operating revenues were a first quarter record $6.3 billion, a 10.9 percent increase, year-over-year

First quarter 2024 RASM was flat, year-over-year—at the low end of the Company’s previous guidance range

The Company had record first quarter revenue performance driven by strong demand trends and record first quarter passenger and ancillary revenue, passengers carried, and new Rapid Rewards® Members. The Company’s first quarter 2024 RASM came in at the low end of its expectations primarily due to lower-than-expected close-in leisure passenger volume, including lower-than-expected maturation of development markets. Still, nominal sequential RASM in first quarter 2024 was ahead of normal seasonal trends. First quarter 2024 managed business revenues strengthened sequentially, as expected, finishing roughly flat when compared with first quarter 2019 levels, and up approximately 25 percent, year-over-year. Network optimization adjustments, implemented with the March schedule, were accretive and supported the profitability inflection point and strong margins for the month of March 2024.

Based on current booking trends, the Company continues to expect an all-time quarterly record for operating revenue in second quarter 2024. Second quarter 2024 RASM is expected to decrease in the range of 1.5 percent to 3.5 percent, on capacity growth of 8 percent to 9 percent, both year-over-year. The comparison includes just over one point of year-over-year headwind from the combined impact of Easter and 4th of July timing. Once again, the Company currently expects nominal second quarter 2024 sequential RASM trends to exceed normal seasonal trends. This anticipated sequential improvement includes expected benefits from revenue initiatives—most notably a full quarter of network optimization.

Significant challenges presented by Boeing aircraft delivery delays, and the related reduction in second half 2024 capacity, negatively impact the Company’s previous expectation for double-digit year-over-year operating revenue growth for full year 2024. As such, the Company now expects full year 2024 year-over-year operating revenue growth approaching high-single digits when adjusted for current trends and planned reductions for post-summer schedules. While the Company remains committed to the goal of earning its cost of capital, these new challenges, combined with current trend pressures, make it more realistic to expect that to occur beyond 2024. The Company is working on further optimization of its network with the goal to improve unit revenue performance and operating margins5. To that end, the Company has made the difficult decision to cease operations at Bellingham International Airport, Cozumel International Airport, Houston’s George Bush Intercontinental Airport, and Syracuse Hancock International Airport on August 4, 2024, and significantly restructure other markets, most notably by implementing capacity reductions in both Hartsfield-Jackson Atlanta International Airport and Chicago O’Hare International Airport.

The Company’s initiatives, which include the estimated benefit of network changes, are expected to contribute between $1.0 billion and $1.5 billion in 2024 year-over-year pre-tax profits, compared with its initial plan of roughly $1.5 billion. The estimated value has been updated for first quarter actual performance, development market adjustments, and capacity changes in the second half of the year. Furthermore, the Company will continue to evaluate its network and work on its robust set of new strategic initiatives, including revenue generating opportunities.

Fuel Costs and Outlook:

First quarter 2024 economic fuel costs were $2.92 per gallon1—slightly below the Company’s previous expectations primarily as a result of lower-than-expected refinery margins—and included $0.08 per gallon in premium expense and $0.04 per gallon in favorable cash settlements from fuel derivative contracts

First quarter 2024 fuel efficiency improved 2.5 percent, year-over-year, primarily due to more -8 aircraft, the Company’s most fuel-efficient aircraft, as a percentage of its fleet

As of April 18, 2024, the fair market value of the Company’s fuel derivative contracts settling in second quarter 2024 through the end of 2026 was an asset of $270 million

The Company’s multi-year fuel hedging program continues to provide protection against spikes in energy prices. The Company’s current fuel derivative contracts contain a combination of instruments based on West Texas Intermediate and Brent crude oil, and refined products, such as heating oil. The economic fuel price per gallon sensitivities3 provided in the table below assume the relationship between Brent crude oil and refined products based on market prices as of April 18, 2024.

Estimated economic fuel price per gallon, including taxes and fuel hedging premiums

Average Brent Crude Oil price per barrel

2Q 2024

2024

$70

$2.45 – $2.55

$2.50 – $2.60

$80

$2.65 – $2.75

$2.70 – $2.80

Current Market (a)

$2.70 – $2.80

$2.70 – $2.80

$90

$2.80 – $2.90

$2.85 – $2.95

$100

$3.00 – $3.10

$3.05 – $3.15

$110

$3.10 – $3.20

$3.15 – $3.25

Fair market value of fuel derivative contracts settling in period

$27 million

$109 million

Estimated premium costs

$39 million

$158 million

(a) Brent crude oil average market prices as of April 18, 2024, were $87 and $84 per barrel for second quarter and full year 2024, respectively.

In addition, the Company is providing its maximum percentage of estimated fuel consumption6 covered by fuel derivative contracts in the following table:

Period

Maximum fuel hedged percentage (a)

2024

58 %

2025

47 %

2026

26 %

(a) Based on the Company’s current available seat mile plans. The Company is currently 55 percent hedged in second quarter 2024 and 58 percent hedged for second half 2024.

Non-Fuel Costs and Outlook:

First quarter 2024 operating expenses increased 12.2 percent, year-over-year, to $6.7 billion

First quarter 2024 operating expenses, excluding fuel and oil expense, special items, and profitsharing1, increased 16.5 percent, year-over-year

First quarter 2024 CASM-X increased 5.0 percent, year-over-year—better than the Company’s previous expectations

The Company’s first quarter 2024 CASM-X increased 5.0 percent, year-over-year, approximately one point better than prior guidance primarily due to favorable airport settlements and higher-than-expected participation in voluntary time off programs. The majority of the first quarter CASM-X increase, year-over-year, was attributable to higher 2024 overall labor cost increases, as well as pressure from planned maintenance expenses.

The Company continues to expect similar cost pressures throughout the year, driving second quarter 2024 CASM-X to an expected increase in the range of 6.5 percent to 7.5 percent, year-over-year. The Company expects full year 2024 CASM-X to increase in the range of 7 percent to 8 percent, based on a reduction of roughly 2 points of lower than previously expected capacity, on a year-over-year basis.

First quarter 2024 net interest income, which is included in Other expenses (income), increased $18 million, year-over-year, primarily due to a $16 millionincrease in interest income driven by higher interest rates.

Fleet, Capacity, and Capital Spending: During first quarter 2024, the Company received five -8 aircraft and retired three -700 aircraft, ending first quarter with 819 aircraft. Given the Company’s discussions with Boeing and expected aircraft delivery delays, the Company plans for approximately 20 -8 aircraft deliveries in 2024, a reduction from the Company’s previous expectation of 46 -8 aircraft deliveries, which differs from its contractual order book displayed in the table below. Consequently, to support fleet flexibility for 2025, the Company plans to retire approximately 35 aircraft in 2024 (31 -700s and four -800s), a reduction from its previous expectation of 49 (45 -700s and four -800s). This will result in a fleet of roughly 802 aircraft at year-end 2024. As a result of Boeing’s delivery delays, the Company has conservatively re-planned its capacity and delivery expectations for the remainder of this year and next. However, there is no assurance that Boeing will meet this most recent delivery schedule.

The Company’s flight schedule is published for sale through March 5, 2025. In light of the Company’s lower aircraft delivery expectations, the Company estimates second quarter 2024 capacity to increase in the range of 8 percent to 9 percent; third quarter 2024 capacity to increase in the low-single digits; fourth quarter 2024 capacity to decrease in the low- to mid-single digits; and full year 2024 capacity to increase approximately 4 percent, all on a year-over-year percentage basis. While the Company continues to adjust and re-optimize schedules for the second half of the year, the current expectation is for aircraft seats and trip frequency to decline in the third and fourth quarters of 2024, both on a year-over-year basis. The Company currently plans for capacity growth beyond 2024 to be at or below macroeconomic growth trends until the Company reaches its long-term financial goal to consistently achieve after-tax return on invested capital (“ROIC”)7 well above its weighted average cost of capital (“WACC”).

The Company’s first quarter 2024 capital expenditures were $583 million, driven primarily by aircraft-related capital spending, as well as technology, facilities, and operational investments. The Company now estimates its 2024 capital spending to be roughly $2.5 billion, which includes approximately $1.0 billion in aircraft capital spending, assuming approximately 20 -8 aircraft deliveries in 2024 and continued progress delivery payments for the Company’s contractual 2025 firm orders.

Last week, the Company entered into a Supplemental Agreement with Boeing relating to its contractual order book for -7 and -8 aircraft. This Supplemental Agreement addresses updates related to the continued -7 delay in certification and supports the Company’s continued focus on fleet modernization. The Supplemental Agreement formalized the conversion of 19 2025 -7 firm orders into -8 firm orders as of March 31, 2024, and shifted one 2025 -8 option into 2026 as of April 2024. The following tables provide further information regarding the Company’s contractual order book and compare its contractual order book as of April 25, 2024, with its previous order book as of January 25, 2024. The contractual order book as of April 25, 2024 does not include the impact of delivery delays and is subject to change based on ongoing discussions with Boeing.

Current 737 Contractual Order Book as of April 25, 2024:

The Boeing Company

-7 Firm Orders

-8 Firm Orders

-7 or -8 Options

Total

2024

27

58

—

85

(c)

2025

40

19

14

73

2026

59

—

27

86

2027

19

46

25

90

2028

15

50

25

90

2029

38

34

18

90

2030

45

—

45

90

2031

45

—

45

90

288

(a)

207

(b)

199

694

(a) The delivery timing for the -7 is dependent on the FAA issuing required certifications and approvals to Boeing and the Company. The FAA will ultimately determine the timing of the -7 certification and entry into service, and the Company therefore offers no assurances that current estimations and timelines are correct.

(b) The Company has flexibility to designate firm orders or options as -7s or -8s, upon written advance notification as stated in the contract.

(c) Includes five -8 deliveries received year-to-date through March 31, 2024. Given the Company’s continued discussions with Boeing and expected aircraft delivery delays, the Company is currently planning for approximately 20 -8 aircraft deliveries in 2024.

Previous 737 Order Book as of January 25, 2024 (a):

The Boeing Company

-7 Firm Orders

-8 Firm Orders

-7 or -8 Options

Total

2024

27

58

—

85

2025

59

—

15

74

2026

59

—

26

85

2027

19

46

25

90

2028

15

50

25

90

2029

38

34

18

90

2030

45

—

45

90

2031

45

—

45

90

307

188

199

694

(a) The ‘Previous 737 Order Book’ is for reference and comparative purposes only. It should not be relied upon. See ‘Current 737 Contractual Order Book’ for the Company’s current aircraft order book.

Liquidity and Capital Deployment:

The Company ended first quarter 2024 with $10.5 billion in cash and cash equivalents and short-term investments, and a fully available revolving credit line of $1.0 billion

The $921 million reduction in cash and cash equivalents during first quarter 2024 was driven primarily by the $1.35 billion payout of the Pilot contract ratification bonus

The Company continues to have a large base of unencumbered assets with a net book value of approximately $17.2 billion, including $14.4 billion in aircraft value and $2.8 billion in non-aircraft assets such as spare engines, ground equipment, and real estate

The Company had a net cash position8 of $2.5 billion, and adjusted debt to invested capital (“leverage”)9 of 47 percent as of March 31, 2024

The Company returned $215 million to its Shareholders through the payment of dividends during first quarter 2024

The Company paid $8 million during first quarter 2024 to retire debt and finance lease obligations, consisting entirely of scheduled lease payments

Awards and Recognitions:

Named to FORTUNE’s list of World’s Most Admired® Companies; ranked #39 overall

Named Domestic Carrier of the Year by the Airforwarders Association

Named the #2 domestic airline by the 2024 Elliot Readers’ Choice Awards

Recognized by Newsweek as one of America’s Most Responsible Companies

Earned Top Score in Human Rights Campaign Foundation’s 2023-2024 Corporate Equality Index

Designated one of the 25 Best Companies for Latinos to Work 2024 by Latino Leaders Magazine

Received the following 2024 designations from Viqtory: Military Friendly Employer, Military Spouse Employer, and Military Friendly Supplier Diversity Program

Environmental, Social, and Governance (“ESG”):

Announced the launch of Southwest Airlines Renewable Ventures (“SARV”), a wholly-owned subsidiary of Southwest Airlines® dedicated to creating more opportunities for Southwest to obtain scalable sustainable aviation fuel (“SAF”), a critical component in the success of the carrier’s goal to replace 10 percent of its total jet fuel consumption with SAF by 2030

Announced the acquisition of SAFFiRE Renewables, LLC (“SAFFiRE”) as part of the SARV investment portfolio. SAFFiRE expects to utilize technology developed at the Department of Energy’s National Renewable Energy Laboratory (“NREL”) to convert corn stover, a widely available agricultural residue feedstock in the U.S., into renewable ethanol

Announced a $30 million investment in LanzaJet, Inc., a SAF technology provider and producer with the world’s first ethanol-to-SAF commercial plant, as part of the SARV investment portfolio

Joined the Hawai’i Seaglider Initiative to explore the feasibility of 100 percent electric, zero direct emissions technology

Published the Southwest Airlines Climate Advocacy statement

Celebrated Black History Month and Women’s History Month throughout February and March 2024, respectively. Southwest highlighted its Employee Resource Groups and encouraged Employees to get involved and learn more about cultural, heritage, and pride months

Highlighted National Human Trafficking Prevention Month to educate Employees and Customers on ways to help combat this issue. Southwest is proud to support multiple nonprofit organizations whose efforts help with the rescue, recovery, and restoration of human trafficking survivors

Launched applications for the Southwest Scholarship Program, which includes two scholarship opportunities. The Southwest Airlines® Community Scholarship seeks to build a diverse talent pipeline, while inspiring future generations to find careers within the airline industry. The Southwest Airlines® Founders Scholarship was established for eligible dependents of Southwest Airlines Employees to pursue higher education

Celebrated the fifth anniversary of Southwest’s service to Hawaii by announcing a partnership with the Council for Native Hawaiian Advancement (“CNHA”) as Presenting Sponsor of the community’s beloved and revitalized Kilohana Hula Show

Visit southwest.com/citizenship for more details about the Company’s ongoing ESG efforts

Because of the Boeing delivery delays, Southwest will drop service to four destinations on August 4, 2024:

Southwest Airlines has announced that its Flight Attendants, represented by the Transport Workers Union Local 556, voted in favor of a new collective bargaining agreement. In addition to industry-leading compensation increases, the new agreement incorporates refined on-call scheduling for Southwest Airlines® Flight Attendants and other quality-of-life enhancements, including Company-paid maternity and parental leaves.

The contract covering nearly 20,000 Southwest® Flight Attendants becomes amendable in 2028.

Since October 2022, 11 union-represented workgroups at the airline have ratified new agreements:

Appearance Technicians

Customer Service Agents, Customer Representatives, and Source of Support Representatives

Hawaiian Holdings, Inc., parent company of Hawaiian Airlines, Inc. reported its financial results for the first quarter of 2024.

“Mahalo to our team for remaining focused on delivering strong operational performance and unparalleled guest experience,” said Hawaiian Airlines President and CEO Peter Ingram . “2024 is off to a positive start as we work to start realizing the return on significant investments we’ve made in our business, including rolling out high-speed Starlink WIFI and taking delivery of our first Boeing 787.”

First Quarter 2024- Key Financial Metrics and Results

GAAP

YoY Change

Adjusted (a)

YoY Change

Net Loss

($137.6M)

($39.3M)

($143.5M)

($31.7M)

Diluted EPS

($2.65)

($0.74)

($2.77)

($0.60)

Pre-tax Margin

(23.7) %

(3.2) pts.

(24.8) %

(1.8) pts.

EBITDA

($109.0M)

($20.8M)

($116.0M)

($12.6M)

Operating Cost per ASM

15.72¢

5.9 %

11.82¢

7.1 %

Operating Revenue per ASM

12.78¢

2.6 %

N/A

N/A

(a) See Table 4 for a reconciliation of adjusted net loss, adjusted diluted EPS, adjusted pre-tax margin, adjusted EBITDA, and adjusted operating cost per ASM (CASM excluding fuel and non-recurring items) to each of their respective most directly comparable GAAP financial measure.

The first quarter loss per share includes ($0.32) per share due to the reduction in the Company’s effective tax rate from 21% to 10%. As of 3/31/2024, the Company has generated federal and state net operating losses (NOLs) of approximately $451 million and $969 million , respectively, which will be used to reduce future cash tax obligations. Analysis under GAAP required us to increase the valuation allowance related to the NOLs which resulted in a lower effective tax rate for the period, decreasing our GAAP tax benefit.

Statistical data, as well as a reconciliation of the reported non-GAAP financial measures, can be found in the accompanying tables.

First Quarter 2024 Highlights

Merger Update

The Company’s stockholders voted in favor of the merger with Alaska Air Group, Inc. (” Alaska “)

The Company and Alaska entered into a timing agreement with the Department of Justice (“DOJ”) in which they agreed not to consummate the merger before 90 days following the date on which both parties have certified substantial compliance with the DOJ’s second request for additional information

Liquidity and Capital Resources

As of March 31, 2024, the Company had:

Unrestricted cash, cash equivalents and short-term investments of $897 million

Liquidity of $1.15 billion , including an undrawn revolving credit facility of $235 million

Outstanding debt and finance lease obligations of $1.75 billion

Routes and Network

Began Boeing 787-9 Dreamliner revenue service on April 15, 2024

Announced new flying from Salt Lake City (SLC) to Honolulu (HNL) and Sacramento (SMF) to Lihu`e (LIH) and Kona (KOA)

Announced increased summer flights between HNL and Austin (AUS), Boston (BOS), Las Vegas (LAS) and Pago Pago (PPG)

Hawaiian will also add a fourth daily flight between HNL and Los Angeles (LAX) from May 24 through September 2

Hawaiian received its second A330-300 freighter from Amazon which will operate between New York’s JFK and San Bernardino (SBD)

Guest Experience

Starlink inflight connectivity is now available free of charge on board all 18 A321neo aircraft

Expanded Premium Airport Service product in its Honolulu hub, offering seamless curb-to-aircraft experience with access to new airport private suite, Apt. 1929

Signed a multi-year distribution agreement with Sabre that will provide Sabre-connected agencies with long-term access to the carrier’s HA Connect™ NDC and traditional EDIFACT content through the Sabre travel marketplace.

Workforce Development

Partnered with Universal Technical Institute , the transportation, skilled trades and energy education division of UTI, Inc. to expand career opportunities for Universal Technical Institute airframe and powerplant graduates who earn their FAA certifications.

Second Quarter 2024 Outlook

The table below summarizes the Company’s expectations for the quarter ending June 30, 2024 expressed as an expected percentage change compared to the results for the quarter ended June 30, 2023 . Figures include the expected impacts of the Company’s freighter operation, which are not yet expected to be material.

Item

GAAP Second Quarter 2024 Guidance

Non-GAAP Equivalent

Non-GAAP Second Quarter 2024 Guidance

Available Seat Miles (ASMs)

Up 3.5% to up 6.5%

Operating Revenue per ASM (RASM)

Down 1.5% to up 1.5%

Costs per ASM (CASM)

Up 8.4% to up 10.7%

CASM excluding fuel and non-recurring items (a)

Up 5.0% to up 8.0%

Gallons of Jet Fuel Consumed (b)

Up 2.5% to up 5.5%

Average fuel price per gallon, including taxes and delivery (c)

$2.83

Economic Fuel Price per Gallon (a)(b)(c)

$2.85

Effective Tax Rate

~10%

Full Year 2024 Outlook

The table below summarizes the Company’s updated expectations for the full year ending December 31, 2024 expressed as an expected percentage change compared to the results for the year ended December 31, 2023 . Figures include the expected impacts of the Company’s freighter operation as the Company establishes its freighter operation.

Item

Prior GAAP Full Year 2024 Guidance

Updated GAAP Full Year 2024 Guidance

Non-GAAP Equivalent

Prior Non-GAAP Full Year 2024 Guidance

Updated Non-GAAP Full Year 2024 Guidance

Available Seat Miles (ASMs)

Up 6.0% to up 9.0%

Up 4.5% to 7.5%

Costs per ASM

Up 0.7% to up 3.0%

Up 4.1% to up 6.3%

CASM excluding fuel and non-recurring items (a)

Flat to up 3.0%

Up 1.0% to up 4.0%

Gallons of Jet Fuel Consumed (b)

Up 4.0% to up 7.0%

Up 3.0% to up 6.0%

Average fuel price per gallon, including taxes and delivery (c)

$2.55

$2.80

Economic Fuel Price per Gallon (a)(b)(c)

$2.59

$2.83

Capital Expenditures

$500M to $550M

No change

(a) See Table 3 and Table 4 for a reconciliation of CASM excluding fuel and non-recurring items and economic fuel price per gallon to each of their respective most directly comparable GAAP financial measures.

(b) Gallons of jet fuel consumed do not include fuel used in the freighter operation, as those expenses are pass-through expenses not born by the Company.

(c) Average fuel price per gallon and economic fuel price per gallon estimates are based on the April 10, 2024 fuel forward curve.

Volaris (Mexico City) will become a publicly-owned company. The Mexican carrier has issued this statement:

Volaris has announced it has priced its initial public offering comprised of 61,992,540 Series A shares for the Mexican offering and 226,469,000 Ordinary Participation Certificates (CPOs) in the form on American Depositary Shares (ADSs) for the international offering at an initial offering price of Ps.15.51 per Series A share and U.S. $12.00 per ADS. Each ADS represents 10 CPOs and each CPO represents a financial interest in one Series A share of common stock of the Company. Shares are expected to begin trading on the Mexican Stock Exchange (BMV) and the New York Stock Exchange (NYSE), under the symbols “VOLAR” and “VLRS”, respectively.

Deutsche Bank Securities Inc., Morgan Stanley & Co. Incorporated and UBS Securities, LLC acted as international joint bookrunners; Santander Investment Securities Inc. and the before mentioned acted as joint local bookrunners. Santander, Evercore, Barclays Capital Inc., and Cowen and Company, LLC served as international co-managers; Evercore Casa de Bolsa, S.A. de C.V.and Barclays served as local co-managers.

Copyright Photo: Juan Carlos Guerra/AirlinersGallery.com. Airbus A319-133 XA-VOP (msn 4403) in the promotional Puebla livery departs from the Mexico City hub.

TAP Portugal (Lisbon) posted a $20.6 million profit in 2012.

The airline issued the following financial statement:

With a profit of 15.9 million euros in 2012, this was well above the 3.1 million in 2011, TAP SA achieved positive results for the fourth consecutive year.

In 2012, total debt was reduced from 1042 TAP million to 862 million, which represents an improvement of 21%. Note also that the total debt, which in 2011 represented 46% of total income and gains, fell to 35% in 2012.

Obtaining a positive net income for the fourth year was made possible by the company’s growth, which reached 4.4% with over 10,186 million passengers, surpassing for the first time in its history the barrier of 10 million.

Total revenues in financial year 2012 amounted to 2,429 million euros, showing an increase of 6.9% compared to 2273 million in the previous year, highlighting the Maintenance Assistance (Third Party) with an improvement of 23% and ticket revenues with a growth of 6.7%.

Operating costs, excluding fuel, stood at 1,422 million euros, 4.8% more than the 1,357 recorded in 2011. The fuel bill, whose cost has not stopped growing since 2008, had in 2012 an additional 93 million euros, up 13% compared to 2011.

The positive results of TAP reflect the continuing effort to improve efficiency, achieved through productivity gains and decreased consumption.

Operating results were also positive at 43.4 million euros, 5.6% better than the 41.1 recorded in 2011.

While increasing the supply (PKO) 4.1%, the national airline increased demand (PKU) of 4.8%, which allowed also improve the load factor of 76.3% in 2011 to the 76.8 percent in 2012.

Copyright Photo: Dave Glendinning. Airbus A320-214 CS-TNP (msn 2178) in the Star Alliance livery taxies to the runway at London (Heathrow).

You must be logged in to post a comment.